Residential Conveyacing

TBC does not generally undertake residential conveyancing but will on occasion provide this service to our business clients.

The buying and selling of properties can be a stressful and worrying time but clear explanations and basic understanding of the process can make the experience less stressful.

The Parties.

1. The Buyer/Purchaser: the person who is looking to buy the property

2. The Estate Agent: the person who markets the property for sale on behalf of a Seller/Vendor

3. The Mortgage Broker: the person who arranges a loan (Mortgage) for a Buyer who is buying the property

4. The Seller/Vendor: the person selling the property

5. The Solicitors/Lawyers: instructed to act on behalf of the Seller and the Buyer. In this context, a conveyancer is a specialist lawyer who specialises in the legal aspects of buying and selling real property, or conveyancing

The Initial Process

Normally, a Seller wishing to sell a property will use the services of an Estate Agent to market the property for sale. This is often done by the agent advertising the property online, in the window display of his offices and by placing a For Sale board outside the property. Sometimes a sale may not involve any agents.

The Buyer will see the property being advertised, will arrange a viewing through the agent and if satisfied make an offer to purchase the property by offering the full asking price or a price lower than the Seller indicated.

Accepting does not mean that there is any commitment by the Seller to sell or the Buyer to buy the property and the matter remains subject to a formal exchange of contracts. This is the stage at which the Lawyers are instructed.

The Seller‘s Solicitors will prepare the contracts for the sale of the property evidencing the Seller’s legal title to the property, and provide the Buyer with the information about the property.

The Buyer‘s Solicitor, on receipt of the Seller‘s contracts and papers will apply for various searches of the Local Authority.

The Buyer will need to ensure, that they have the necessary finance to purchase the property and if not, will need to apply for a mortgage (loan) from a Bank or Mortgage Company. It is important for a Buyer to ensure, that on completion they will have all the necessary funds not only to complete the transaction, but to pay for the stamp duty and land registration fees.

The Exchange

Once all the papers are received by the Buyer‘s Solicitor, including the results of the searches related to the property, and the Buyer’s mortgage offer (loan offer) from a Bank or Mortgage company, the Buyer‘s Solicitor will send the Buyer a report. A Buyer‘s Solicitor must have his Client‘s mortgage offer, a signed contract and the Buyers 10% deposit, before contracts are exchanged.

Once the contract is agreed and the Buyer is happy with the report, the Buyer‘s Solicitor will contact the Seller‘s Solicitor to fix a completion date.

The Completion

Following an exchange of contracts, the Buyer’s Solicitor sends a report to the Buyer‘s lenders requesting the monies in time for the completion, prepares a statement for the Buyer so that the Buyer is aware of the balance required for the completion. The Seller in readiness for completion will sign the Transfer Document and his Solicitor will apply to his mortgage company for a figure which will need to be paid if there is a mortgage.

On the date fixed for the completion, the Buyer‘s Solicitor will pay the Seller‘s Solicitor the required sum. When the payment is made the keys are handed over or released by the Seller to the Buyer through the offices of the Estate Agent. The Seller‘s Solicitor use that sum to pay off any debt or mortgage on the property and the Buyer will pay the stamp duty and will apply to register the Transfer and the Mortgage Deed.

The entire Buying and Selling process will take between six and eight weeks, but that estimated timescale depends on various factors such as :

1. The Seller and the Buyer instructing their Solicitors and satisfying the firm‘s compliance requirements;

2. The time it takes for papers to be received from the Seller‘s Solicitor;

3. The time it would take for the results of searches undertaken by the Buyer’s Solicitor;

4. The length and the time for a mortgage offer to be issued to the Buyer;

5. Whether the Seller has a property which he is buying there by the transaction becoming a chain in which case the entire transaction is determined by a formation of that chain so that on an agreed date, the contracts for all the properties in that chain are exchanged and completed simultaneously.

A Property transaction doesn‘t only involve a sale or a purchase but may also involve a property being refinanced with other lender or being transferred without it being a sale or a purchase, often referred to as a transfer of equity .

TBC is not CQS accredited and will be on a restricted panel of lenders who will instruct the firm to act on their behalf in the transaction. Where the firm is not on a panel of lender, the lender will instruct an independent law firm to act on his behalf.

At TBC we believe that independence and the provision of independent legal advice is a hallmark of transparency.

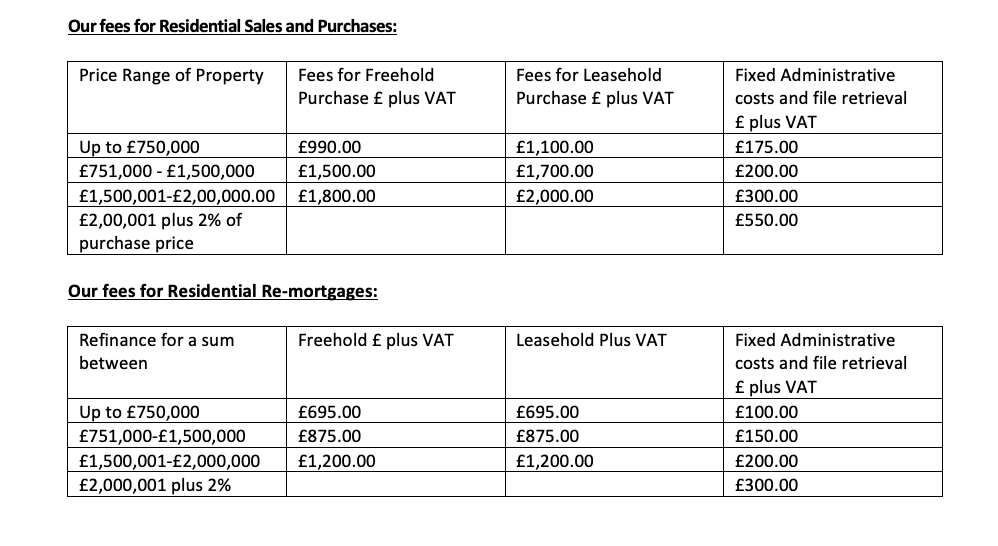

As a firm, we undertake matters on a fixed fee basis provided that everything goes as agreed. In the event that the matters becomes complicated or unduly protracted we reserve the right to a proportionate increase of our fees which we will notify you about in writing, including the justification of any such increase.

The Fixed Administrative costs are part of our fees but we show them separately as we do the same in our accounting records. They are not a disbursement.

Disbursement

These are payments we are obliged to make on your behalf to third parties during the transactions:

1. Fees to HM Land Registry for a document of title searches and Land Registry fees in the case of the latter, namely Land registry fees these are set by the government and can be seen on the Land Registry website which has a very simple to use calculator. Scale one applies to the fees payable on a purchase and scale two where there is a refinance involved: see fee calculator here.

2. Fees paid for searches undertaken. The cost of these depends on where the property is located and the search company used. All our searches are undertaken by a company called Land Mark. Whatever sum they charge us is passed on to you as a disbursement.

3. Stamp duty is payable within 15 days of the completion date, not paying attracts a penalty and interest. It is important that when purchasing a property, that you as the Buyer immediately return the Stamp Duty Land Tax (SDLT) form on or before completion to so that it can be filed on time. A Stamp duty calculator can be found on the HMRC website here.

4. Payment to an insurance company may also be required – when there are defects in title or where there is lack of planning and these are required to be obtained for the benefit of any lender or your benefit. We will notify you about the cost involved .

The process of purchasing a leasehold property compared to a freehold one is similar – in the case of a leasehold the lease is also checked and the landlord pack obtained, and both are also reported on.

We do not consider transfers of equity, whether in divorce proceedings (where the property is transferred from joint names into one of the parties’ name as part of the financial settlement), or where this is required as part of a family or other arrangement, to fall under the above fee scale. The fees payable in such instances would depend on whether the consent for such a transfer is required from any registered lender, and whether the manner in which you wish to hold the property is to be determined by a Trust Deed.

![]() These transfers of equity if undertaken where a property is mortgage with the consent of the mortgagee may attract stamp duty, depending on the amount of the loan outstanding. The transfer will also attract a Land Registry fee depending on the value of the property. These payments will be disbursement.

These transfers of equity if undertaken where a property is mortgage with the consent of the mortgagee may attract stamp duty, depending on the amount of the loan outstanding. The transfer will also attract a Land Registry fee depending on the value of the property. These payments will be disbursement.